Student Loan Forgiveness is Robbing Peter to Pay Paul

With President Biden’s Saving on a Valuable Education (SAVE) plan set to extend more student loan relief to borrowers this summer, the federal government is pretending it can wave a magic wand to make debts disappear. But the truth of student debt “relief” is that they’re simply shifting the burden to everyone else, robbing Peter to pay Paul and funneling more steam into an inflation pressure cooker that’s already set to burst.

Starting July 1st, new rules go into effect that change the discretionary income requirements for their payment plans from 10% to only 5% for undergraduates, leading to lower payments for millions. Some borrowers will even have their owed balances revert to zero.

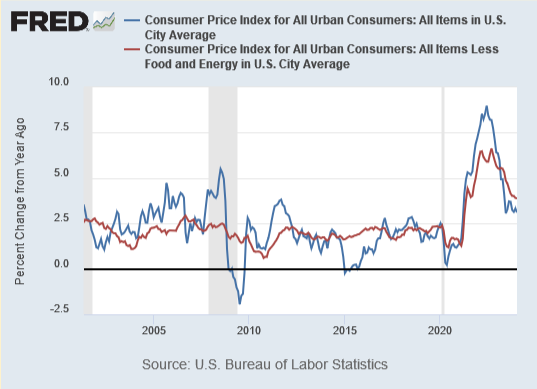

What the plan doesn’t describe, predictably, is how that burden will be shifted to the rest of the country by stealing value out of their pockets via new taxes or increased inflation, which still simmering well above levels seen in early 2020 before the Fed printed trillions in Covid “stimulus” money. They’re rewarding students who took out loans they can’t afford and punishing those who paid their way or repaid their loans, attending school while living within their means. And they’re stealing from the entire country to finance it.

Biden actually claims that a continuing Covid “emergency” is what gives him the authority to offer student loan forgiveness to begin with. As with any “temporary” measure that gives state power a pretense to grow, or gives them an excuse to collect more revenue (I’m looking at you, federal income tax), COVID-19 continues to be the gift that keeps on giving for power and revenue-hungry politicians even as the CDC reclassifies the virus as a threat similar to the seasonal flu.

The SAVE plan takes the burden of billions of dollars in owed payments away from students and adds it to a national debt that’s already ballooning to the tune of a mind-boggling trillion dollars every 3 months. If all student loan debt were forgiven, according to the Brookings Institution, it would surpass the cumulative totals for the past 20 years for multiple existing tax credits and welfare programs:

“Forgiving all student debt would be a transfer larger than the amounts the nation has spent over the past 20 years on unemployment insurance, larger than the amount it has spent on the Earned Income Tax Credit, and larger than the amount it has spent on food stamps.”

Ironically enough, adding hundreds of billions to the national debt from Biden’s program is likely to cause the most pain to the very demographics the Biden administration claims to be helping with its plan: poor people, anyone who skipped college entirely or paid their loans back, and other already overly-indebted young adults, whose purchasing power is being rapidly eroded by out-of-control government spending and central bank monetary shenanigans. It effectively transfers even more wealth from the poor to the wealthy, a trend that Covid-era measures have taken to new extremes.

As Ron Paul pointed out in a recent op-ed for the Eurasia Review:

“…these loans will be paid off in part by taxpayers who did not go to college, paid their own way through school, or have already paid off their student loans. Since those with college degrees tend to earn more over time than those without them, this program redistributes wealth from lower to higher income Americans.”

Even some progressives are taking aim at the plan, not because it shifts the debt burden to other Americans, but because it will require cutting welfare or sacrificing other expensive social programs promised by Biden such as universal pre-K. For these critics, the issue isn’t so much that spending and debt are totally out of control, but that they’re being funneled into the wrong issues.

Progressive “solutions” always seem to take the form of slogans like “tax the wealthy,” a feel-good bromide that for lawmakers always seems to translate into increased taxes for the middle and lower-upper class. Meanwhile, the .01% continue to avoid taxes through offshore accounts, money laundering trickery dressed up as philanthropy, and general de facto ownership of the system through channels like political donations and aggressive lobbying.

If new waves of college applicants expect loan forgiveness plans to continue, it also encourages schools to continue raising tuition and motivates prospective students to continue with even more irresponsible borrowing. This puts pressure on the Fed to keep interest rates lower to help accommodate waves of new student loan applicants from sparkly-eyed young borrowers who figure they’ll never really have to pay the money back.

With the Fed already expected to cut rates this year despite inflation not being properly under control, the loan forgiveness scheme is just one of many factors conspiring to cause inflation to start running hotter again, spiraling out of control, as the entire country is forced to pay the hidden tax of price increases for all their basic needs.

Related Posts

To Prevent a Banking Crisis, the FED Must Cut

In 2009, 140 banks failed, and a recent report from financial consulting firm Klaros Group says that hundreds of banks are at risk of going under this year. It’s being billed mostly as a danger for individuals and communities than for the broader economy, but for stressed lenders across America, a string of small bank failures could quite […]

In 2009, 140 banks failed, and a recent report from financial consulting firm Klaros Group says that hundreds of banks are at risk of going under this year. It’s being billed mostly as a danger for individuals and communities than for the broader economy, but for stressed lenders across America, a string of small bank failures could quite […]Inflation Brewing: Is Coffee the Next Cocoa?

Cocoa prices have dumped since rocketing to a dramatic peak last month as an El Nino cycle winds down and traders rush out of the illiquid market. For now, depreciating fiat currencies are still keeping the cocoa price still far above its 2023 levels. Coffee has had a similar rise and subsequent correction — but now, inflation and other factors are conspiring to […]

Cocoa prices have dumped since rocketing to a dramatic peak last month as an El Nino cycle winds down and traders rush out of the illiquid market. For now, depreciating fiat currencies are still keeping the cocoa price still far above its 2023 levels. Coffee has had a similar rise and subsequent correction — but now, inflation and other factors are conspiring to […]California’s Single-Family Zoning Exemplifies the Market-Intervention Problem

California’s government bet that they knew better than the free market. And now millions are paying the price. The story begins in 1919, when the city of Berkley, California instituted legislation setting aside districts that would only allow the construction of single-family housing. The idea spread, and soon much of California’s urban areas had adopted the zoning policy. Today, approximately 40% of the total land in Los Angeles is […]

California’s government bet that they knew better than the free market. And now millions are paying the price. The story begins in 1919, when the city of Berkley, California instituted legislation setting aside districts that would only allow the construction of single-family housing. The idea spread, and soon much of California’s urban areas had adopted the zoning policy. Today, approximately 40% of the total land in Los Angeles is […]“Safe Haven” Yen Trending Towards Zero Against Gold

The yen was once known as a safe-haven currency for investors to protect themselves when broader markets are shaky or other currencies are dropping, but those days are numbered. A stable government and consistent (and low) interest rates have been some of the driving factors, but it’s the unwinding of that ultra-low interest rate policy that will be the yen’s “safe […]

The yen was once known as a safe-haven currency for investors to protect themselves when broader markets are shaky or other currencies are dropping, but those days are numbered. A stable government and consistent (and low) interest rates have been some of the driving factors, but it’s the unwinding of that ultra-low interest rate policy that will be the yen’s “safe […]Made in America: The Dark Forces Promoting American Manufacturing

Whenever an election year rolls around, domestic manufacturing becomes a more central theme of discussion. Candidates from both sides, who seem to disagree on almost everything else, never waver in their commitment to auto manufacturers in Detroit and the steel industry. Republicans and Democrats never forget to remind the American public that they will try […]

Whenever an election year rolls around, domestic manufacturing becomes a more central theme of discussion. Candidates from both sides, who seem to disagree on almost everything else, never waver in their commitment to auto manufacturers in Detroit and the steel industry. Republicans and Democrats never forget to remind the American public that they will try […]