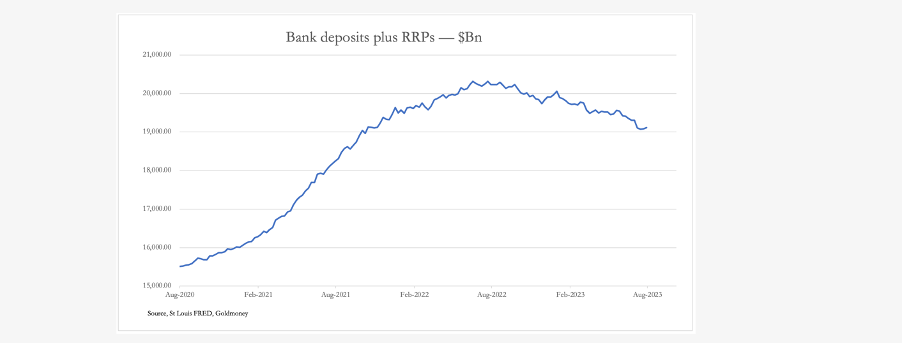

Globally, further falls in consumer price inflation are now unlikely and there are yet further interest rate increases to come. Bond yields are already on the rise, and a new phase of a banking crisis will be triggered.

This article looks at the factors that have come together to drive interest rates higher, destabilising the entire global banking system. The contraction of bank credit is in its early stages, and that alone will push up interest costs for borrowers. We have an old-fashioned credit crunch on our hands.

Dishonest money is destroying our standard of living.

What do I mean by “dishonest” money?

I mean government fiat money that it can create out of thin air. This is inflation and it constantly eats away our purchasing power.

Good news! The recession is off!

For months, economists predicted the Federal Reserve’s rate hikes to fight price inflation would spin the US economy into a recession. But there is a growing consensus that the central bank can slay price inflation while guiding the economy to a “soft landing.”

Economists Bob Murphy and Jonathan Newman say, “Not so fast!”

In another sign the financial crisis continues to bubble under the surface, banks borrowed an additional $3.7 billion from the Federal Reserve’s bank bailout program in July.

Currently, there are $106.9 billion in outstanding loans in the Bank Term Funding Program (BTFP).

The Consumer Price Index (CPI) data for July came out last week. Even though the headline number ticked up slightly compared to June, most mainstream analysts took it as a sign that the Federal Reserve made more progress in its inflation fight. In fact, most mainstream pundits seem convinced that the Fed is on the verge of winning that fight and pushing CPI back to its 2% target. In his podcast, Peter said they are wrong.

Credit cards are great until the bill comes due. And the US economy has about maxed out the plastic. The Federal Reserve incentivized borrowing and the economy is buried under trillions of dollars in debt. As Friday Gold Wrap host Mike Maharrey explains in this episode, the bill is about to come due. He also goes over the July CPI data and digs into some of the ramifications.

After the Federal Reserve incentivized borrowing with more than a decade of artificially low interest rates and easy money, the debt chickens are coming home to roost.

Last week, Fitch Ratings downgraded the US’s long-term credit rating from AAA to AA+, and on Monday, Moody’s cut the credit rating of 10 small and midsize banks.

The Federal Reserve advertises itself as “independent” and above the political fray.

The Fed is inherently political and makes decisions based on political calculations as much as economic data.

Is price inflation really heading back toward the Federal Reserve’s 2% target?

Most people in the mainstream seem to think so, and the recent drop in the consumer price index (CPI) appears to support this belief. Price inflation has trended downward over the last several months, with the annual CPI falling from a high of 9% last year to just 3% in July. But I don’t think the Fed has won the inflation fight and I don’t believe the central bank’s sanguine inflation outlook is correct.

I think easing price inflation is transitory.

JP Morgan forecasts $2,000 gold by the end of the year with the price continuing to rise to record highs in 2024.

In his latest note, JP Morgan executive director of global commodities research Greg Shearer projects the price of gold will average around $2,175 an ounce by the fourth quarter of 2024. That would represent an 11% increase from the current price.