All Eyes on Switzerland This Sunday

Switzerland will vote on the “Save Our Swiss Gold” initiative this Sunday, and the news is reminding everyone just why the financial world is watching so closely. USA Today and the Wall Street Journal can give you a good summary of how the Swiss gold initiative would affect the policies of the Swiss National Bank (SNB). The Guardian explains why a “yes” vote on the initiative would be extremely bullish for gold in this article published yesterday:

Its supporters come from the populist right-wing Swiss People’s party (SVP), which says in its mission statement: ‘Most Swiss don’t even know that part of the nation’s gold is stored abroad and that the SNB has already sold over half of the gold reserves.’

“Switzerland, a country with a strong tradition of refining and trading gold, has the highest gold reserves per inhabitant of any country, equivalent to four ounces a head. For many this remains insufficient.

If the Swiss vote yes on Monday, the SNB would be required to buy 1,500 tonnes of gold over the next five years, the equivalent of almost 70% of the global gold mined every year. Experts say the gold price would soar. ‘It would be an unforgettable day for the precious metal industry,’ according to German business analyst Michael Schröder.”

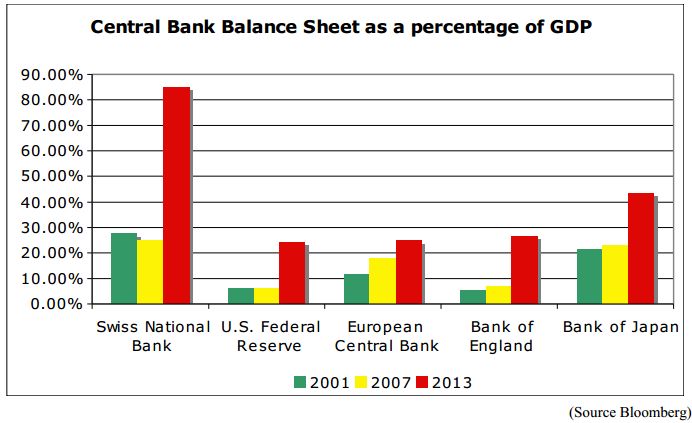

Of course, the SNB is terrified of the initiative passing. The bank’s main argument against the gold referendum is that it would make it too difficult for the central bank to conduct its monetary policy, particularly the trick of pegging the Swiss franc (CHF) to the euro through its “minimum exchange rate.” This sounds important, and central bankers are great at spinning stories that make their monetary manipulation sound essential and complex.

However, the real effects on the Swiss economy of pegging the CHF to the euro are easily understood. The following piece by Eric Schreiber explains the history of the peg, which has lead to the now dangerously high balance sheet the SNB. While a bit technical, Schreiber deftly counters the SNB’s argument against a “yes” vote while emphasizing the symbolic importance of this vote in rebalancing the power of the people versus the banking elite.

The SNB’s primary objections to the gold initiative are three fold. 1) It claims that gold is ‘one of the most volatile and riskiest investments’, 2) that a 20% gold requirement will lower the ‘distributions to the confederation and the cantons’ since gold does not pay interest like bonds and dividend paying stocks, and 3) that the 20% gold holding requirement will interfere with its ability to conduct monetary policy and complicate efforts to maintain ‘the minimum exchange rate’, the ‘temporary’ policy of pegging the Swiss franc (CHF) to the Euro (EUR) it initiated in 2011 and continues to enforce to this day.

“The first two concerns can quickly be addressed and discounted. Gold is indeed a volatile asset at times but so are bonds and equities. In recent years Greek, Spanish, Italian, Irish and other European bonds have been far more volatile than gold. The SMI, the Swiss stock index, lost over 50% of its value on two separate occasions between 2000 and 2009 while gold steadily rose at an annual rate of 8.50% over the same period.

“Regarding the second concern, the distribution of proceeds derived from financial speculation and paid to the confederation and cantons, one has to question whether or not it is really appropriate for the SNB to re-brand itself as a hedge fund instead of remaining focused on its core responsibilities as a central bank.

“To properly address the third SNB concern requires a historical context and a more detailed analysis. Prior to the change in the Swiss constitution, the CHF was backed by a minimum amount of 40% gold. Despite this constraint, Swiss monetary policy at the SNB was unhindered and functioned properly during the post World War II period. The SNB is correct in implying that today a partial gold backing, as required by the referendum, would make its policy of weakening the CHF against the EUR more difficult. Although the SNB has raised the currency peg as a reason for voting against the referendum the issue has not been directly addressed by the ‘YES’ camp. Is the peg necessary? Does the population in Switzerland benefit as a whole from a weak EURCHF exchange rate? Why does the SNB feel compelled to continue a policy that it characterized over 3 years ago as ‘temporary’? How did “the minimum exchange rate” policy come to be? Why hasn’t there been a public debate about it?”

Get Peter Schiff’s latest gold market analysis – click here – for a free subscription to his exclusive weekly email updates.

Interested in learning more about physical gold and silver?

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Related Posts

Why and How US Debt Will End in Catastrophe

As fiscal imbalances persist, driven by coercive measures and artificial currency creation, the middle class faces erosion and purchasing power dwindles. But as the world hurtles towards a potential reckoning, the lingering question remains: can this precarious balance last, or are we teetering on the brink of a cataclysmic economic shift?

As fiscal imbalances persist, driven by coercive measures and artificial currency creation, the middle class faces erosion and purchasing power dwindles. But as the world hurtles towards a potential reckoning, the lingering question remains: can this precarious balance last, or are we teetering on the brink of a cataclysmic economic shift?Will the World’s Most Pro-Bitcoin Politician Embrace Gold?

Since Nayib Bukele became president of El Salvador, El Salvador has been in American media and global political discussion more than ever. While much of the attention focuses on Bukele’s mass incarceration of gang members and a decline in homicide of over 70%, Bukele has also drawn attention to his favoritism towards Bitcoin and how he […]

Since Nayib Bukele became president of El Salvador, El Salvador has been in American media and global political discussion more than ever. While much of the attention focuses on Bukele’s mass incarceration of gang members and a decline in homicide of over 70%, Bukele has also drawn attention to his favoritism towards Bitcoin and how he […]The Economy Is Reaching a Tipping Point

Beneath the veneer of headline job gains, the American economy teeters on the brink: native employment dwindles as part-time and immigrant jobs surge. Government hiring camouflages looming recession warnings. Inflation and political blunders worsen the crisis, fueling public outrage at the establishment’s mishandling of the economy.

Beneath the veneer of headline job gains, the American economy teeters on the brink: native employment dwindles as part-time and immigrant jobs surge. Government hiring camouflages looming recession warnings. Inflation and political blunders worsen the crisis, fueling public outrage at the establishment’s mishandling of the economy.Prices Up 2500% Since FDR Abandoned Gold

On April 5 1933, Franklin D. Roosevelt abandoned the gold standard, wielding questionable legal power amidst America’s dire economic depression. His whimsical approach to monetary policy, including coin flips and lucky numbers, unleashed unprecedented inflation and price increases that have since amounted to nearly 2500%. Our guest commentator explores this tragic history and the legacy […]

On April 5 1933, Franklin D. Roosevelt abandoned the gold standard, wielding questionable legal power amidst America’s dire economic depression. His whimsical approach to monetary policy, including coin flips and lucky numbers, unleashed unprecedented inflation and price increases that have since amounted to nearly 2500%. Our guest commentator explores this tragic history and the legacy […] With gold hitting yet another awe-inspiring all-time high in the wake of Powell’s remarks reassuring markets (more or less) to expect rate cuts in 2024, a few analysts are pointing out risk factors for a correction — so is there really still room to run?

With gold hitting yet another awe-inspiring all-time high in the wake of Powell’s remarks reassuring markets (more or less) to expect rate cuts in 2024, a few analysts are pointing out risk factors for a correction — so is there really still room to run?

Leave a Reply