Leveraged Loan Market Comes Unglued

As WolfStreet put it, the $1.3 billion leveraged loan market has come unglued.

“Leveraged loans” are made to firms already deeply in debt. Think subprime loans for corporations. As with any risky loan, they could be difficult to either collect or resell in a downturn, putting both the borrower and lender at risk.

According to the S&P/LSTA Leveraged Loan Index, the total leveraged loan market has doubled since 2008 and has grown by about 17% this year alone. A record 59% of these loan rate B+ or worse, according to S&P Global. According to the credit rating agency, “Risks attributable from this debt binge are significant.”

But the current problem isn’t that these highly leveraged, negative cash flow companies are defaulting on these risky loans — not yet. The problem is that investors are fleeing the loan mutual funds that were super-hot investments for years.

This is a proverbial canary in a coal mine.

According to WolfStreet, investors pulled $3 billion out of loan mutual funds and $300 million out of exchange-traded loan funds during the week ended December 19. That $3.3 billion ranked as the largest outflow on record, according to Lipper. The previous record was $2.5 billion yanked out the week before. It was the fifth week in a row of net outflows exceeding $1 billion — another record. And since the week ended October 31, net outflows totaled $11.3 billion.

WolfStreet said investors are fleeing in droves hoping to grab the “first-mover advantage” in an illiquid market.

They want to be the first out the door before they get caught in a run-on-the-fund – with potentially catastrophic consequences for their cherished money.”

When investors start fleeing from these loan mutual funds, it creates a sort of snowball effect, as WolfStreet explains.

Loan-mutual funds sit on some cash with which to meet redemptions because selling a loan to meet redemptions can take a long time even in good times, but investors can get out of a mutual fund with the click of a mouse. This ‘liquidity mismatch’ is very risky: When redemptions pick up momentum, the fund becomes a forced seller into an illiquid market where only a few vulture hedge funds (set up precisely for that opportunity) are willing to buy at cents on the dollar, even if the loans have not yet defaulted. Forced selling, the associated losses, and the inability still to meet redemptions can cause open-end mutual funds, such as these loan funds, to collapse. Now these funds are flooded with record redemptions, and they’re selling loans to stay ahead of redemptions and maintain a cash cushion in order to avoid the fate that afflicted a number of open-end bond mutual funds during the Financial Crisis and during the oil bust a couple of years ago: a collapse of the fund when there is a run-on-the-fund.”

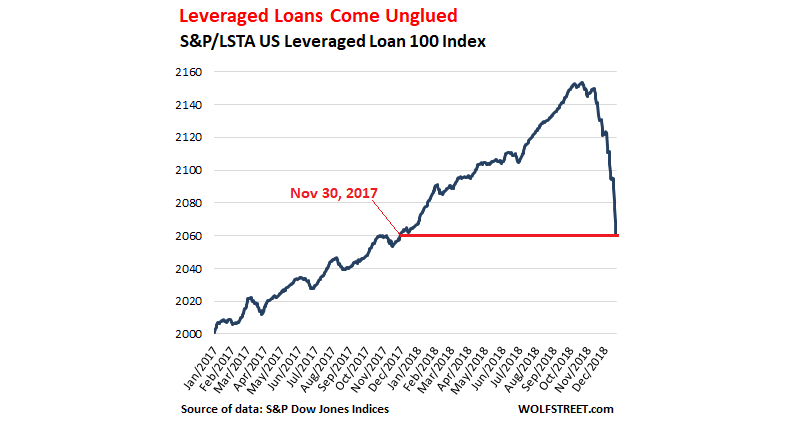

The S&P/LSTA US Leveraged Loan 100 Index tracks the largest and most liquid of these leveraged loans. The index has dropped 4.3% since mid-October. That may not sound like a whole lot until you realize that the price isn’t supposed to drop at all. These loans are investments with a fixed value and rising interest payments. They should increase in value over time. Even so, the past eight weeks of price declines wiped out the gains of the last 11 months.

And the wave of defaults hasn’t even started yet.

And that’s the real risk. Debt-ridden companies will have an increasingly difficult time making loan payments as interest rates continue to climb. If we’re already seeing shakiness in the marketplace, what’s it going to look like when the actual tidal wave of defaults hits? WolfStreet says what we’re seeing today is just the first step.

Credit is tightening, and it will be harder and more expensive for junk-rated companies to refinance existing debts when they come due, and a wave of defaults is expected, but hasn’t happened yet, and the impact of those defaults on leveraged loans is scheduled for later. What we’re seeing now is investors getting cold feet. It’s the first step.”

Get Peter Schiff’s most important Gold headlines once per week – click here – for a free subscription to his exclusive weekly email updates.

Interested in learning how to buy gold and buy silver?

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!