In his most recent Gold Videocast for SchiffGold, Albert K Lu interviewed John Rubino, founder of DollarCollapse.com. Rubino had a pretty compelling explanation for why there wasn’t a massive, sustained economic collapse a decade ago, and why he thinks it’s still lurking on the horizon.

The reason that we’re still here, when we really should have fallen apart based on how much debt there was out there, and various other measures of instability, is that a printing press has turned out to be a great tool for fooling people.”

Rubino pointed out that this is the first time in human history that all of the world’s governments are armed with a basically unlimited fiat currency printing press. The ability to create money out of thin air has allowed governments to take on more debt than anybody imagined feasible. Rubino noted that economists 20 years ago couldn’t have imagined $7 trillion of bonds trading at negative interest rates, and global debt at 300% of global GDP, but that’s where we are today. He went on to explain how the entire world pitched in to help the Federal Reserve keep things limping along after the 2008 meltdown. For instance, post 2009, China borrowed more money than any country has ever borrowed in history.

Rubino said there’s no way to know when the economy will hit the wall, but it will likely be pretty soon. At some point central banks and governments will run out of the ability to borrow and print, and they will have to start living within their means again.

According to Rubino, It’s going to be a painful transition. So, what does this mean for gold? Lu and Rubino share their insights.

This article was submitted by Joel Bauman, SchiffGold Precious Metals Specialist. Any views expressed are his own and do not necessarily reflect the views of Peter Schiff or SchiffGold.

In the last few decades, we have seen an international trend towards a “cashless world.” Physical currency is becoming relatively scarce and the world’s money supply is made up of almost entirely electronic funds. Governments and banks are waging a war on cash and you don’t want to become a victim.

According to the Federal Reserve, in July of 2013, the total amount of physical currency in the world equaled $1.2 trillion, most of it held outside the United States. This accounted for a mere 7.7% of the total $15.5 trillion money supply. (Cash, checking/savings accounts, money market accounts, stocks and bonds) The percentage of physical cash in relation to electronic funds has been steadily decreasing over the last 50 years.

Interestingly, even with the diminishing purchasing power of the US dollar, the face value of Federal Reserve notes has also been decreasing. Today the highest denomination produced by the Federal Reserve is the one hundred dollar note. US currency used to include denominations of $500, $1,000, $5,000, and even $10,000. In 1969, the Federal Reserve began taking these higher denominations out of circulation. Recently, a former US Treasury Secretary floated the idea of doing away with the $100 bill as well.

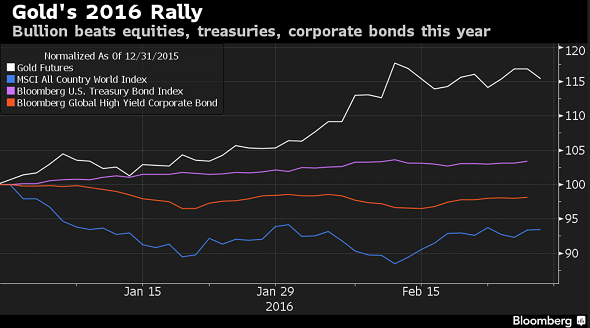

Just a few months ago, mainstream analysts were calling gold a “barbaric relic.” Now all of a sudden, they are saying, “Buy gold!”

Last Friday, Deutsche Bank issued a note asserting that with emerging economic risks and market turmoil, signs point in gold’s favor:

There are rising stresses in the global financial system…Buying some gold as ‘insurance’ is warranted.”

Deutsche Bank isn’t alone in singing gold’s praises. A Bloomberg report crowned gold “the biggest winner of 2016,” noting it’s posted 15% gains so far in 2016:

Turmoil across global equity and currency markets has sparked demand for a haven. Speculators raised their net-long position in gold to the highest in a year.”

The demand for gold and silver bullion coins surged in the last half of 2015, and it has not abated so far this year, despite a rally in the price of both metals.

Last year, demand was so strong the US Mint sold out of American Silver Eagles in July. Inventory was replenished in August, but the coins were on weekly allocations of roughly 1 million ounces for the rest of the year. The mint set a record for Silver Eagle sales in 2015, with the final total coming in at 47 million ounces.

The demand for American Gold Eagles was equally brisk in the last half of 2015. The US Mint announced it had sold out of one-ounce coins in late November and halted production for the year. It sold out of smaller sized Gold Eagles earlier that month.

Despite mounting data pointing toward a recession right around the corner, many mainstream analysts continue to insist that declining stock markets and other signs of economic turmoil are just a blip on the radar and things will quickly turn around.

David Stockman appeared on CNBC’s Futures Now last Friday and blasted this bullish line of thinking, saying we are heading for a global recession and a huge crash in the financial markets. In the process, he hit those optimistic about the economy square in the jaw:

Frankly I think your traders are smoking something stronger than what I can legally buy here in Colorado.”

Despite Stockman’s insistence that the dynamics are all pointing toward a crash, the show host continued to push the narrative that this is just a small bump in the road and ultimately the market will resume its upward trend.

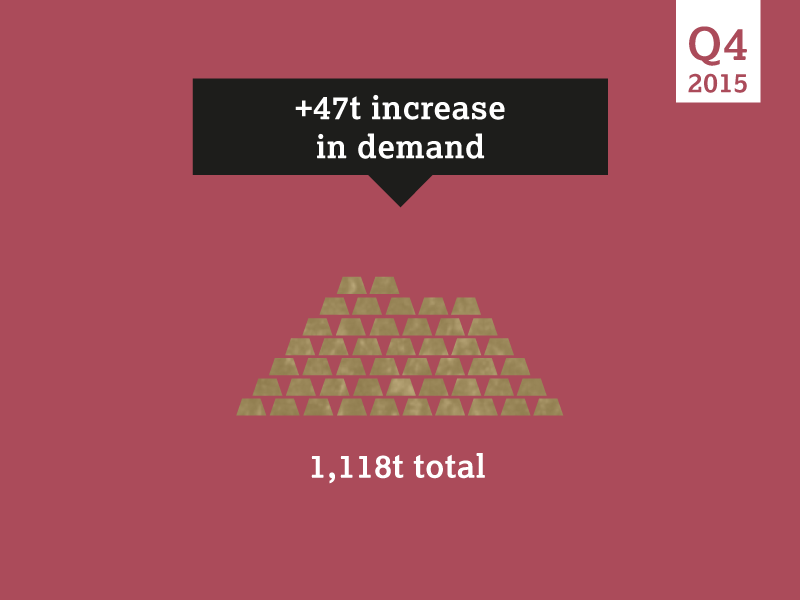

After a tepid first half of 2015, demand for gold rallied during the last half of the year, despite a number of economic and external factors working against it.

According to the World Gold Council’s Gold Demand Trends Full Year 2015 a surge in demand during the fourth quarter turned around what was looking to be a bad year for the yellow metal:

Gold demand in the fourth quarter increased 4% year-on-year to a 10-quarter high of 1,117.7 tons. Full year demand was virtually unchanged…Weakness in the first half of the year was cancelled out by strength in the second half. Fourth quarter growth was driven by central banks (+33 tons) and investment (+25 tons).”

Central bankers want you to think they have all the answers. They talk about their policy “tool kits” as if they can just reach in and find the proper solution for any possible economic scenario.

But if you peer behind the curtain, it becomes apparent they may not really know what they’re doing after all. In fact, with a recession looming on the horizon, there are some signs of desperation among economic central planners.

The conventional Keynesian wisdom that dominates today holds that central banks need to lower interest rates when the economy slumps in order to stimulate borrowing and spending. But rates in the US hover just barely above zero. In the Eurozone and Japan, they languish in negative territory. So, what is a central banker to do when the next recession hits?

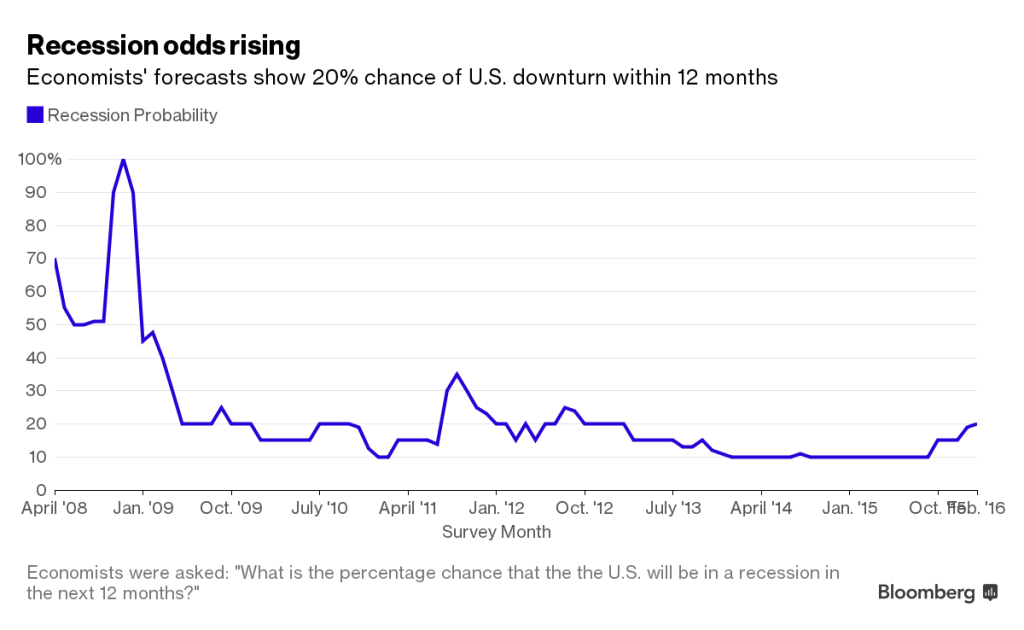

With four states officially in recession, and economic data continuing to point toward a broader downturn, it’s getting increasingly difficult for officials to sell the illusion of a strong US economy.

Peter Schiff has been saying for weeks that the US may already be in a recession. Recently, Jim Grant appeared on CNBC’s Closing Bell and echoed Peter’s sentiments, saying the US likely went into recession in late December. And while officials at the Federal Reserve keep insisting the US economy remains strong, some mainstream analysts have started sounding recession warning bells as well. In fact, the number of mainstream economists predicting a recession within the next 12 months continues to rise.

So far, people have been able to blow off talk of a looming recession as mere chatter, but in some US states, it’s not just speculation; it’s reality. According to a Bloomberg report, four US states have officially gone into recession, with three more “at risk of prolonged declines.”

Could the student loan bubble be on the verge of popping?

If desperate government actions serve as any indication, it may well be.

Last week, seven US Marshals armed with automatic weapons came to Paul Aker’s home in Houston to arrest him for a $1,500 student loan debt dating back to 1987. According to the Guardian, Acker isn’t alone facing the barrel of a gun over outstanding student loans:

Aker is unlikely to be the only person to be surprised by marshals collecting on student loans. A source at the marshal’s office told Fox 26 that it is planning to serve warrants on 1,200 to 1,500 people over student loan debts.”

The war on cash heated up this week when a former Obama economic adviser/ex-Treasury secretary floated the idea of eliminating the $100 bill.

Lawrence Summers called for death to the Benjamins in a post on his Washington Post blog titled It’s Time to Kill the $100 Bill. The post announced the release of a paper by Harvard’s Mossavar Rahmani Center for Business and Government senior Fellow Peter Sands arguing that governments should stop issuing high-denomination currency such as 500 euro notes and $100 bills. The paper even proposed withdrawing such currency them from circulation.

Cash warriors always publicly center their arguments on the need to limit cash as a way to fight drug crime, terrorism, and tax fraud. This was exactly how Summers framed the argument in his blog post: