What Do You Mean “No Inflation?”

When the Fed launched its aggressive monetary policy in the wake of the 2008 financial crisis, many free-market economists predicted it would result in massive price inflation. That never materialized. As a result, Keynesian economists like Paul Krugman love to finger-point and mock those who criticize easy money policies designed to “stimulate aggregate demand.” They claim the lack of price inflation proves they were right all along. You can massively increase the money supply during a downturn to stimulate the economy without sparking inflation. Free-market people are wrong.

But just because we don’t see price inflation doesn’t mean there isn’t any inflation at all. After all, the new money has to go someplace. If we don’t see it manifested in rising prices, it’s because we’re looking in the wrong place.

In response to the Great Recession, the Federal Reserve plunged interest rates to near zero and held them at historically low levels for several years. It also engaged in three rounds of quantitative easing – in essence, printing money out of thin air. Over a span of nearly seven years, the Fed’s balance sheet increased 427%. With all of that new money entering into the economy, one would expect a significant increase in price inflation. And yet the rise in the consumer price index has been muted. In fact, officials at the Federal Reserve constantly fret about the lack of price inflation.

So where did all that money go?

Just look at Wall Street.

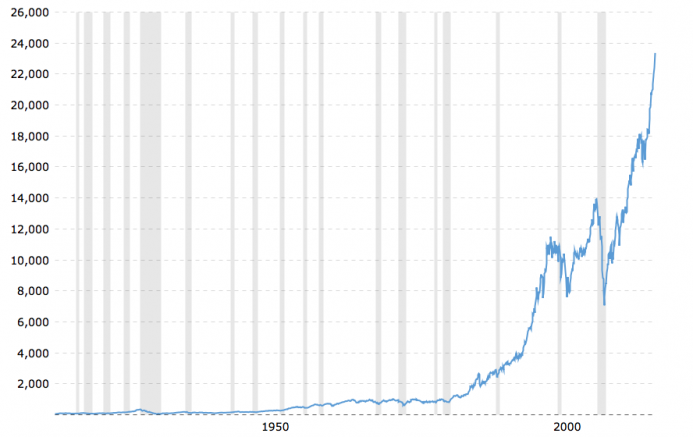

When the Dow Jones hit bottom in the spring of 2009, it was at just under 6600. On Nov 1, 2017, the Dow closed at 23,435.

There’s your inflation.

Otherwise known as a bubble.

C.Jay Engel explained why Fed policy blew up a stock market bubble instead of price inflation in a recent article published on the Mises Wire.

![]()

Now, in a completely free market with sound money that cannot be fractionally lent out or merely created digitally, general prices in the economy would tend to stay relatively stagnant over time or ticking downward as productivity increases. This doesn’t mean prices of individual goods always remain the same, it means that, mathematically, as some prices rise, others must fall. Aggregate prices can only rise over time if there is a constant increase in the supply of money.

This principle includes, of course, stock market prices. That is, if there is no monetary expansion, stock market averages would mathematically not be able to trend upwards, unless people consumed less elsewhere in order to buy stocks. Individual stocks of growing companies could go up while stocks of companies less in tune with consumer demand would fall. But the phenomenon of all stocks across most businesses going up at the same time can only take place in a regime of monetary expansion. For more, see Kel Kelly’s Mises Daily article here.

In the years since the last great inflation scare of the 1970s, we have seen the money supply expand monumentally, while the consumer prices have not gone back to 70s style increases. And indeed, as the Fed quadrupled its balance sheet in response to the financial crisis of 2008, even still: shockingly low consumer price inflation (especially compared to what many thought would happen, given the money supply expansion). But yet, while consumer price inflation rates never hit the same double digits as they did in the 70’s check out the Dow Jones:

What we are seeing here is not a lack of price inflation as the Fed recklessly expands its balance sheet and increases money supply levels beyond what was previously thought inconceivable. What we are seeing is a shift of price inflation away from consumer prices and toward the stock and bond markets.

What caused this shift?

One of the reasons that the inflation has hit asset prices far more intensely than consumer prices is because of how the Central Bankers reacted to the 70’s double-digit price inflation. When Nixon took the United States off the gold standard completely, the result was freedom of the central banks to greatly expand the money supply. The downside of this was that the money quickly entered the hands of the consumers and caused tremendous damage to the currency’s purchasing power. Volker, of course, responded by increasing interest rates quite substantially and killing the rising price inflation.

This created a big problem for governments. Robert Blumen describes this in a Mises Daily article several years ago:

“The conundrum facing governments at the time was how to enable governments to continue to live beyond their means, without suffering inflationary consequences. […] The mechanism of the last major bout of inflation was the sale of government debt to commercial banks. In this process, called “monetization,” banks or the Fed create the money out of nothing with which to purchase the bonds.”

The problem was that the Federal Government wanted the Fed to help finance its reckless spending without actually producing price inflation. The solution to this dilemma is the cause of maniacal stock price booms since the 1990s. It is the reason why the Fed’s massive monetary expansion never resulted in consumer price inflation. The “quantitative easing” embarked on by Bernanke never resulted in extremely high consumer price inflation because the banking system no longer expands the money supply by way of commercial banks.

Instead, as Blumen writes:

the centerpiece of [the central bank solution to the dilemma] was a change in the method of financing government debt. Deficit finance bonds would be sold to private investors through existing financial markets. This would place the bonds in the hands of investment funds, rather than on the books of commercial banks as would have been the case had they returned to the old style of monetization.

[These changes] confined the price adjustments resulting from monetary expansion to the financial system. The character of the 80s and 90s inflation differed from that of the 70s. In recent decades, price changes following money quantity changes have been in stocks and bond prices, rather than wages and consumption goods prices.

![]()

Now the Fed is looking to “normalize” interest rates and shrink its balance sheet. In other words, it is about to cut off the flow of easy money to the financial markets.

What do you think will happen?

Eventually, the air is going to come out of that stock market bubble. In a podcast last month, Peter Schiff questioned why people are so bullish about the Fed’s plans.

I don’t know why the markets are excited about the prospect of a plan to shrink the Fed’s balance sheet, because if the Fed actually shrunk the balance sheet, the markets wouldn’t like it because it would put dramatic upward pressure on interest rates which are not good for stocks.”

So, don’t let the pundits fool you. The lack of price inflation does not mean central bank intervention has had no effect. It has inflated a huge stock market bubble. And at as some point, that thing is going to pop. Ultimately, the Fed’s monetary tightening could become a havoc-wreaking juggernaut.

Get Peter Schiff’s most important Gold headlines once per week – click here – for a free subscription to his exclusive weekly email updates.

Interested in learning how to buy gold and buy silver?

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Related Posts

The Copper Supply Shortage Is Here

With the AI boom and green energy push fueling fresh copper demand, and with copper mines aging and not enough projects to match demand with supply, the forecasted copper shortage has finally arrived in earnest. Coupled with persistently high inflation in the US, EU, and elsewhere, I predict the industrial metal will surpass its 2022 top to reach a […]

With the AI boom and green energy push fueling fresh copper demand, and with copper mines aging and not enough projects to match demand with supply, the forecasted copper shortage has finally arrived in earnest. Coupled with persistently high inflation in the US, EU, and elsewhere, I predict the industrial metal will surpass its 2022 top to reach a […]How Trust (or the lack of it) Affects America’s Trajectory

America’s trust in its institutions has rapidly eroded over the past 20 years. We have a lower level of trust in our judicial system and elections than most European countries. Some of this is natural, as Americans are uniquely individualistic, but much of it arises from repeated government failures.

America’s trust in its institutions has rapidly eroded over the past 20 years. We have a lower level of trust in our judicial system and elections than most European countries. Some of this is natural, as Americans are uniquely individualistic, but much of it arises from repeated government failures.When Will the Yen Carry Trade Break?

Decades of negative interest rate policy in Japan have ended. That could mean the end of the $20 trillion “yen carry trade,” once one of the most popular trades on foreign exchange markets, and a chain reaction in the global economy. The yen carry trade is when investors borrow yen to buy assets denominated in […]

Decades of negative interest rate policy in Japan have ended. That could mean the end of the $20 trillion “yen carry trade,” once one of the most popular trades on foreign exchange markets, and a chain reaction in the global economy. The yen carry trade is when investors borrow yen to buy assets denominated in […] With a hot CPI report casting a shadow of doubt on the likelihood of a June interest rate cut, all eyes are on the Fed. But they’ve caught themselves in a “damned if they do, damned if they don’t” moment for the economy — and the news for gold is good regardless.

With a hot CPI report casting a shadow of doubt on the likelihood of a June interest rate cut, all eyes are on the Fed. But they’ve caught themselves in a “damned if they do, damned if they don’t” moment for the economy — and the news for gold is good regardless. The Educational Gap in Economics

It’s no secret that the American public is wildly ignorant of many issues that are central to the success of our nation. Just a generation ago it would have been unthinkable that less than half of the American population could recognize all three branches of government. America is in most cases far less educated about its government […]

It’s no secret that the American public is wildly ignorant of many issues that are central to the success of our nation. Just a generation ago it would have been unthinkable that less than half of the American population could recognize all three branches of government. America is in most cases far less educated about its government […]